When you buy property in Portugal, there are a few taxes to be aware of upfront. IMT is usually the largest of them, and it surprises buyers who haven’t budgeted for it. Here’s what it is, how it’s calculated, and what you might be able to avoid.

So, what is IMT?

IMT stands for Imposto Municipal sobre as Transmissões Onerosas de Imóveis — which translates roughly as Municipal Tax on Property Transfers. In plain terms, it’s the tax you pay to the Portuguese government when you buy real estate. Think of it as the country’s version of stamp duty land tax in the UK, or transfer tax in other markets.

It’s a one-off payment, settled before the final deed is signed. You won’t pay it again each year; that’s a separate tax called IMI, which we’ll touch on briefly at the end. IMT is purely a purchase cost.

The rate isn’t flat. It depends on three things: the value of the property, whether it’s going to be your primary residence or a second home, and whether it’s located on the mainland or in the Azores or Madeira.

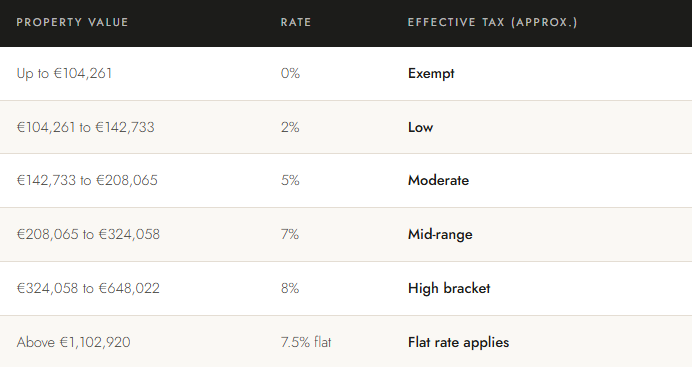

How is it calculated?

Here’s something that catches people out: IMT isn’t always calculated on what you actually pay for a property. It’s calculated on whichever is higher — the declared purchase price in the deed, or the official tax value of the property, known as the VPT (Valor Patrimonial Tributário). In most Algarve transactions, the purchase price is higher, so that’s what gets used. But it’s worth being aware of.

The rates are progressive, meaning they increase in brackets as the property value rises. For a primary residence on mainland Portugal in 2025, the structure looks like this:

For most luxury property purchases in the Algarve, you’ll typically land in the 7% to 8% bracket. The rate applies to the total purchase price but there are fixed deductions built into each band, which means your actual effective rate ends up lower than the headline figure.

A practical example: If you’re buying a villa at €800,000 as a second home, your IMT would be calculated at a flat 8% on that amount. That’s €64,000. For the same property as a primary residence, the calculation uses the progressive band structure with deductions, bringing the figure down noticeably. The distinction between primary and secondary residence matters a great deal here.

Second homes and investment properties

Second homes and rental properties don’t benefit from the primary residence brackets. The rates are slightly different and, importantly, there’s no lower-value exemption. For urban properties being purchased as a holiday home or investment, a flat rate of 8% applies across the board once the value exceeds the first bracket. For rural land, the rate is 5% regardless of intended use.

Commercial properties have their own flat rate of 6.5%, no matter where they are or what they’re worth.

Who might be exempt?

There are a few situations where you can reduce or eliminate IMT entirely.

Young first-time buyers (under 35)

Since August 2024, buyers aged 18 to 35 purchasing their first primary residence can claim a full IMT exemption on properties up to €324,058. If the property is worth more than that — up to €648,022 — a reduced rate of 8% applies with a significant deduction. This applies to the stamp duty as well. It’s a meaningful saving for anyone who qualifies, and it’s not retroactive, so it only applies to deeds signed after 1 August 2024.

Urban rehabilitation

If you’re buying a property in a designated Urban Rehabilitation Area (ARU) with plans to renovate, you may be eligible for an IMT exemption. The property generally needs to be over 30 years old, and the works must begin within three years of purchase. This is more relevant for urban town houses and older village properties than for new Algarve villas, but worth knowing if you’re buying a renovation project.

Buildings of national or public interest

Officially classified heritage buildings are exempt from IMT. If you’re buying a listed property — a quinta with protected status, for example — your lawyer will be able to confirm whether this applies.

When do you pay it?

IMT has to be paid before the final deed is signed. Your Portuguese lawyer (called a solicitador or advogado) will guide you through the process — they’ll calculate the amount due, prepare the relevant forms, and make sure payment is made to the tax authority (Autoridade Tributária) in advance of the notarial appointment.

This isn’t something you can settle later. No payment, no deed. It’s one of the reasons having a good local lawyer is so important when buying in Portugal.

What else do you pay at the same time?

IMT doesn’t come alone. At the same time, you’ll also pay:

Stamp Duty (Imposto do Selo) — a flat 0.8% on the purchase price. It’s modest compared to IMT, but it’s worth factoring in. If you’re taking out a mortgage, there’s an additional stamp duty on the loan itself: 0.5% for loans under five years, or 0.6% for longer terms.

Notary and registration fees — typically around 1% combined, covering the deed itself and the land registry update.

So the full picture of upfront purchase costs, on top of the agreed price, is generally IMT plus roughly 1.8% to 2% more. For a €1 million purchase, that means setting aside somewhere in the region of €80,000 to €90,000 for taxes and fees, depending on how the property is classified.

A note on IMI

Once you own the property, you’ll pay IMI each year — the annual property ownership tax. In most Algarve municipalities, this sits between 0.3% and 0.4% of the property’s VPT (not the market value, which is usually considerably higher). It’s modest by international standards, and nothing like IMT in terms of scale.

Can offshore structures or company purchases change anything?

Buyers sometimes ask about purchasing through a company or offshore structure. The rules here have tightened considerably over the years. Shares in offshore companies that hold Portuguese real estate are still subject to IMT when the shares change hands. Properties held by companies in blacklisted jurisdictions attract a flat IMT rate of 10%. This is an area where you really do need specialist legal and tax advice before structuring anything — the savings, if any exist at all, come with significant compliance obligations.

The bottom line

IMT is not optional and it’s not small. On a luxury property in the Algarve, it will typically represent your biggest single transaction cost after the purchase price itself. The key is knowing about it early, budgeting for it properly, and making sure you understand whether you’re buying as a primary residence or a second home, as that single distinction can change the final number quite significantly.

If you’re unsure what your IMT liability would look like on a specific property, speak to your lawyer before making an offer. And if you don’t yet have a lawyer, our team is happy to point you toward trusted advisors we work with regularly throughout the Algarve.

This article is intended as a general overview for informational purposes only and does not constitute tax or legal advice. Tax rules change, and individual circumstances vary. Always consult a qualified Portuguese tax adviser or solicitor before proceeding with a purchase.